The Corporate Transparency Act (CTA) is a federal law designed to thwart the misuse of anonymous shell companies in the United States. Enacted in January 2021 as part of the National Defense Authorization Act, the CTA represents a crucial step in combating illicit business activities by demanding increased transparency.

According to the Federal Register, over 2 million corporations and limited liability companies are formed in the U.S. each year. Alarmingly, around 10% of these entities are identified for involvement in illegal activities, such as money laundering, fraud, tax evasion, and various other illicit pursuits. The CTA’s primary goal is to reveal the true owners of entities established in the U.S., making it challenging for malicious actors to conceal illicit funds or assets.

The CTA mandates the reporting of substantial beneficial ownership information, requiring corporations, limited liability companies (LLCs), and similar entities registered in the U.S. to disclose their beneficial owners to the Financial Crimes Enforcement Network (FinCEN), a bureau of the U.S. Department of the Treasury.

This legislation has raised several crucial questions for business owners and tax professionals, including: “Who is required to submit a beneficial ownership report?” “What defines a beneficial owner?” “Which businesses are exempt from BOI regulations?” “How can I file a BOI report?”

Using FinCen’s FAQs, let’s break it down.

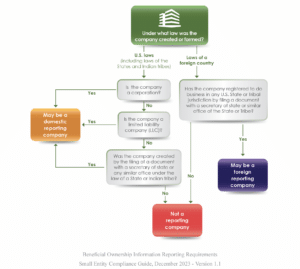

Understanding which companies need to file a beneficial owner report is vital for compliance with regulations set by the FinCEN. These companies, termed “reporting companies,” fall into two categories: domestic reporting companies, created within the United States by filing with a secretary of state or similar office, and foreign reporting companies, formed under foreign laws but registered to do business in the United States. Exceptions exist for 23 types of entities, and careful examination of these exemptions is necessary before concluding that a company is exempt.

The helpful flowchart below, provided in FinCEN’s Small Entity Compliance Guide, assists in identifying reporting companies. Additionally, considerations for specific entity types, such as trusts, depend on state laws regarding the creation or registration of these entities. For instance, a domestic entity like a statutory trust becomes a reporting company only if created by filing with a state office. Similar rules apply to foreign entities, ensuring consistency in reporting obligations across various structures.

Moreover, certain exemptions may apply based on activities, revenue, or other factors. For instance, there are exemptions for inactive entities and those reporting over $5 million in gross receipts or sales, provided they meet other criteria. FinCEN’s guide delves into these exemptions in Chapter 1.2, offering companies insights into potential exemptions and providing clarity on reporting requirements. Sole proprietorships are generally exempt unless created or registered in the U.S. through filing with a secretary of state or similar office.

Certain corporate entities, such as trusts, might not be considered reporting companies if they register with a court of law solely for jurisdictional purposes related to disputes. This nuance clarifies that the mere act of registering for dispute resolution doesn’t trigger reporting obligations. Additionally, the activity or revenue of a company alone doesn’t determine reporting status. Instead, a reporting company is characterized by its creation or registration within the U.S., with specific exemptions applicable based on financial factors.

Even companies created or registered in U.S. territories, including Puerto Rico, the Northern Mariana Islands, American Samoa, Guam, and the U.S. Virgin Islands, are considered reporting companies if they meet specific criteria and don’t qualify for exemptions. This broad territorial scope ensures a comprehensive approach to beneficial ownership reporting, aligning with FinCEN’s commitment to transparency and preventing illicit financial activities.

By carefully navigating FinCen’s guidelines, companies can fulfill their reporting obligations accurately, contributing to the effectiveness of regulatory frameworks and maintaining the integrity of financial systems.

As defined by the Financial Crimes Enforcement Network (FinCEN), a beneficial owner is an individual who either directly or indirectly exercises substantial control over the reporting company or owns at least 25% of its ownership interests. Detailed in FinCen’s Small Entity Compliance Guide, these criteria provide a foundation for identifying beneficial owners and ensuring compliance.

The concept of substantial control, outlined by FinCEN, encompasses various aspects, such as holding senior officer positions, authority in appointing or removing officers, being an important decision-maker, or any other form of significant influence. This multifaceted definition emphasizes the need for a nuanced understanding of an individual’s role within a reporting company. Additionally, exceptions to the beneficial owner definition exist, allowing reporting companies to exclude specific individuals, as detailed in FinCEN’s guidelines.

Special rules come into play when reporting owners who exclusively hold their ownership interests through exempt entities, and distinctions are made regarding the roles of unaffiliated companies in day-to-day operations. As these regulations evolve, staying informed about FinCEN guidelines remains crucial for accurate and timely reporting. By navigating these nuances, reporting companies contribute to the transparency and integrity of financial systems, aligning with the overarching goal of preventing illicit activities within the corporate sphere.

Not all companies fall under the scope of the CTA. Exempted companies include larger organizations with existing statutory obligations to provide regular information updates to the government, such as publicly traded companies, banks, credit unions, investment advisors, insurance companies, or entities in specific regulated industries. Additionally, nonprofits, dormant companies, and companies with over 20 full-time employees in the U.S. that have filed income tax returns demonstrating more than $5 million in gross receipts or sales are exempt.

It’s essential to note that these exemptions may not be permanent, and companies must meet specific criteria outlined in the CTA to qualify. Exemptions may change from company revenue or employee size increasing or decreasing, revised regulations or policy shifts, requiring continuous vigilance from companies that believe they fit into these exemption categories.

For several exempted entities, especially larger organizations with comprehensive regulatory structures, the exemption isn’t solely based on size and industrial standing. It also considers the notion that they are less likely to be used for illicit activities due to rigorous regulatory scrutiny and compliance obligations. This deems their transparency sufficient, eliminating the need for additional beneficial ownership reporting.

Ultimately, the implementation of beneficial ownership reporting under the Corporate Transparency Act primarily targets smaller, privately held entities where the risk of obscurity and potential misapplication is higher.

To navigate the reporting of beneficial ownership information to FinCEN, companies must adhere to specific timelines and procedures outlined by regulatory guidelines.

For reporting companies created or registered before January 1, 2024, the deadline for filing the initial BOI report is January 1, 2025. However, entities created or registered between January 1, 2024, and January 1, 2025, have a 90-calendar day window after receiving notice or public notice of their creation or registration. Reporting companies established on or after January 1, 2025, must file their initial BOI reports within 30 calendar days of receiving actual or public notice that their company’s creation or registration is effective.

FinCEN commenced accepting BOI reports on January 1, 2024, and the submission must be made electronically through the secure filing system provided on FinCEN’s BOI E-Filing website (https://boiefiling.fincen.gov). The process ensures the security and efficiency of reporting, maintaining the integrity of the collected information.

Entities required to report their beneficial ownership information can access the necessary form through FinCEN’s BOI E-Filing website (https://boiefiling.fincen.gov) under the “File BOIR” section.

While there is no requirement for reporting companies to engage an attorney or certified public accountant (CPA) for submission, FinCEN acknowledges that professional service providers can offer valuable assistance.

The submission of BOI reports allows for flexibility in filers. Anyone authorized by the reporting company, whether an employee, owner, or third-party service provider, can file the report on the company’s behalf. When submitting the BOI report, individual filers must provide basic contact information, including their name and contact details.

In summary, understanding the reporting timeline, utilizing the secure electronic filing system, and accessing available resources are key components in ensuring smooth compliance with FinCEN’s beneficial ownership information reporting requirements. Companies are encouraged to familiarize themselves with the guidelines and utilize verified providers and tools to facilitate accurate and timely submissions.

As businesses navigate the intricate requirements of the Corporate Transparency Act, leveraging advanced tools becomes essential for a seamless and compliant process. Recognizing this need, FileForms offers a state-of-the-art software solution designed by licensed attorneys and CPAs, providing a secure and efficient means to file Beneficial Ownership Information Reports.

By choosing FileForms, businesses can streamline the submission of accurate and comprehensive information about beneficial owners and other relevant details, aligning with the transparency goals set by the CTA. Our mission is not only to facilitate compliance but also to contribute to fortifying the integrity of the U.S. economic framework.

In the evolving regulatory landscape, FileForms remains committed to staying abreast of changes and updates, ensuring that our users stay well-informed and prepared for any modifications to the CTA requirements. As businesses embrace the principles of transparency and accountability, FileForms serves as a reliable partner, empowering them to navigate regulatory complexities with confidence.

Choose FileForms for a secure, efficient, and tailored solution to file your BOI Report, ensuring peace of mind every step of the way.